In the previous edition of al-Madinah, we discussed the ruling of investing in the stock market and the different opinions of contemporary jurists regarding it. In short, some contemporary jurists prohibit investing in the stock market since most (if not all) publicly traded companies are involved in some level of sharia non-compliant activity. Whereas many contemporary jurists allow investing in publicly traded companies provided the amount of sharia non-compliance is “negligible”. Thereafter, these jurists laid out conditions of investing in the stock market for the purpose of having clear benchmarks for what constitutes as “negligible”. Those conditions and benchmarks will be discussed below. It should be noted that for the sake of brevity we will only be discussing those conditions which are applicable to publicly traded stocks. Other conditions which practically do not occur or would likely only be applicable to private equity will not be mentioned.

Condition #1: The haram revenue of the company should not exceed 5% of its gross revenue

Reasoning: The contemporary jurists who permit investing in publicly traded stocks do so only if the amount of sharia non-compliant revenue is negligible. Although there are varying views as to what constitutes negligible, many scholars have agreed to the 5% benchmark. The reason for choosing 5% is since this is the amount which is considered negligible in finance. This is derived from an accounting principle which is known as the “Materiality Principle” in which amounts under 5% are generally considered negligible.

Practical application: To assess whether a stock is sharia compliant, a person would look at the sources of revenue in a company’s annual or quarterly report (known in the United States as 10-K or 10-Q filings). These reports can easily be found online through a Google search. Any amount of revenue earned from impermissible sources should be added up. If the total amount of non-compliant revenue exceeds 5% of gross revenue, the stock would not be permissible to invest in. Consider the below example from the 10-K report of Blink Charging (BLNK: NASDAQ):

The only clearly non-compliant revenue is the interest earned by the company. When the interest earned is added to the total revenue (6,230,231 + 16,442), the total revenue becomes 6,246,673. The amount earned through interest is only 0.26% of gross revenue (16,442/6,230,231 x 100= 0.26). Therefore, the condition of non-compliant revenue being under 5% would be fulfilled.

Condition #2: The interest-bearing debt to market cap ratio should not exceed 33%

Reasoning: It is impermissible for a company to take an interest-bearing loan. The Messenger of Allah s cursed any individual involved in interest. Consider the following hadith:

‘Abdullah ibn Mas’ud R narrates that the Messenger of Allah s said, “May Allah’s curse descend upon the one who receives interest, pays interest, becomes a witness (to such a transaction), or even transcribes it.” (Tirmizi)

Since a company’s board of directors act on behalf of the shareholders, the shareholders would indirectly be involved in such non-compliant loans. However, since the involvement is indirect and not at the explicit direction of each individual shareholder, contemporary jurists have permitted “negligent” amount of such non-compliance.

The threshold of “negligent amount” was set to under 33% based on the hadith in which the Messenger of Allah s permitted the bequeathment of up to 33% of one’s assets after their death with the remainder being distributed to the heirs. The Messenger of Allah did not allow the bequeathment of more than 33% and said, “One-third is a large amount”. Contemporary jurists deduced from this hadith that in relation to financial assets one-third or less is a marginal amount, whereas more than one-third would be considered a non-negligible amount from a Sharia perspective.

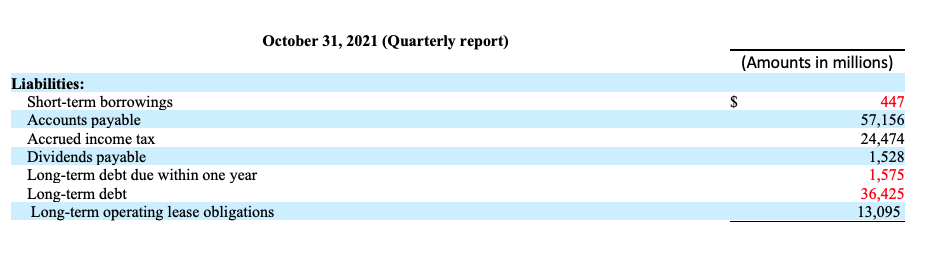

Practical application: When looking at a company’s quarterly or annual financial report, one would immediately scroll down and look for the company’s liabilities. Thereunder, one will find “notes payable”, “borrowing”, or “debt” (different companies may have slightly different wordings on their balance sheet). It is safe to assume that all forms of debt would be interest-bearing, therefore one would add such loans up and see if the total amount of interest-bearing debt is more than 33% of the company’s market cap (total value of company shares). The market cap of a company can easily be found through a Google search as well. Consider the following example from a recent Walmart quarterly report:

From the above liabilities, we find that there are three loans: 447 million, 1.5 billion, and 36.4 billion which amounts to a total of roughly 38.34 billion dollars of interest-bearing debt. The market cap of Walmart (at the time of writing) is 386 billion dollars. The total interest-bearing debt to market cap ratio equates to under 10% (38.34/386 x 100= 9.9%). Therefore condition #2 is fulfilled.

Condition #3: The interest-bearing securities to market cap ratio should not exceed 33%

Reasoning: Interest-bearing securities refer to loans or assets through which the company receives interest. Like the previous condition, the reasoning for why this would be an issue from a sharia perspective is because the company board of directors act on behalf of the shareholders. Therefore, the shareholder would indirectly be involved in such activity. A negligible amount of indirect involvement would be overlooked. The threshold of what constitutes a negligible amount was set to under 33% for the reasons mentioned previously.

Practical application: When looking at a company’s quarterly or annual financial report, one would look under the company’s assets and look for “cash and cash equivalents”. Since companies would normally deposit their cash in an interest-bearing account, it would be safe to assume that this would qualify as an interest-bearing security. If the total amount of interest-bearing securities is less than 33% of a company’s market cap, this condition would be fulfilled.

Note:

From a practical perspective, the above three conditions are usually enough to screen a stock and check for its compliance/non-compliance. Although other conditions have been mentioned in more detailed works on Islamic finance, they have been left out due to being of rare occurrence, only being applicable to private equity, or redundant. Also, it should be noted that the purpose of this article is just to have a peak into what goes into the screening process for stocks. There are different standards of tolerable non-compliance in stocks which have been adopted by various jurists.

Lastly, it is not practical to expect every individual to be able to screen stocks themselves. Individuals may refer to other scholars or apps endorsed by scholars which provide stock screening services.